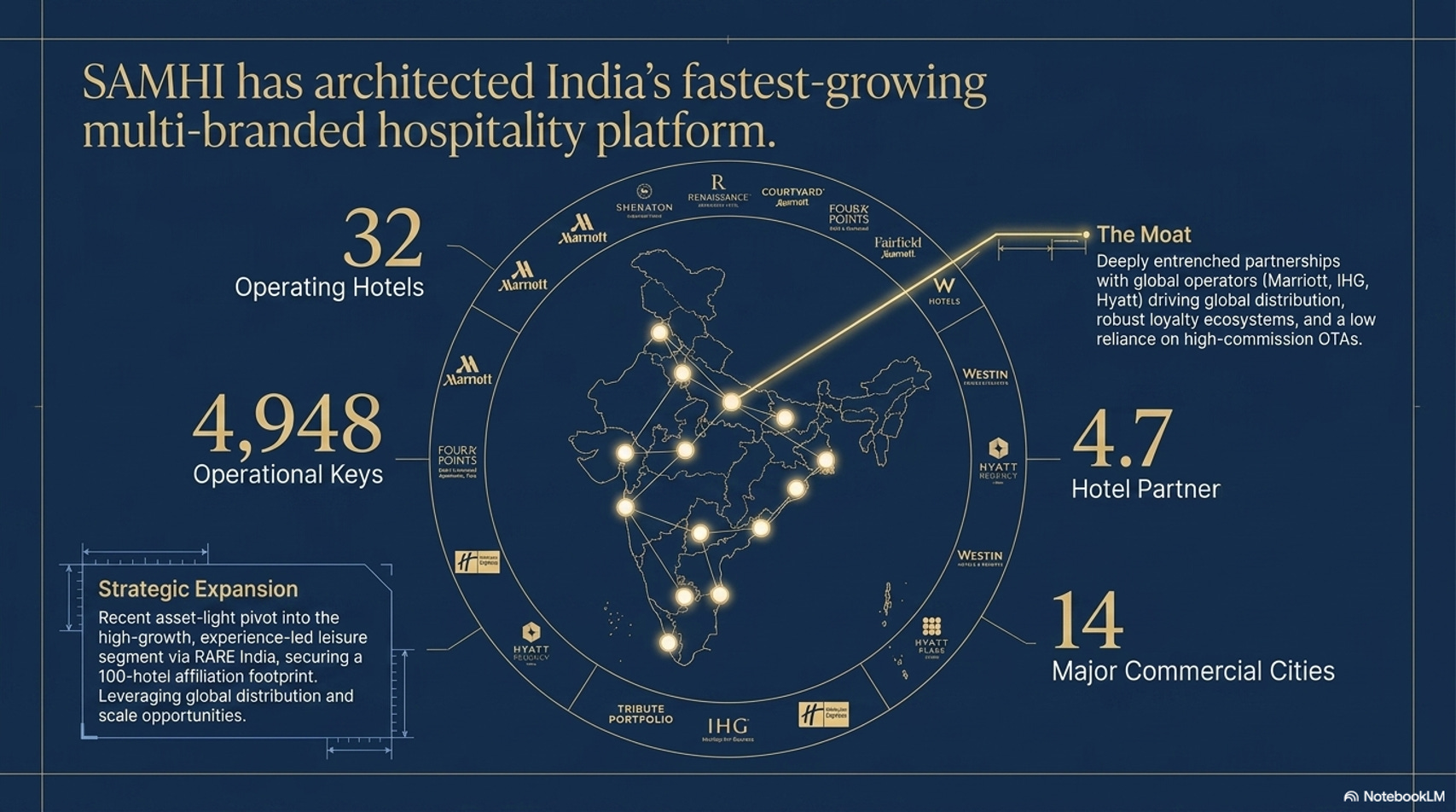

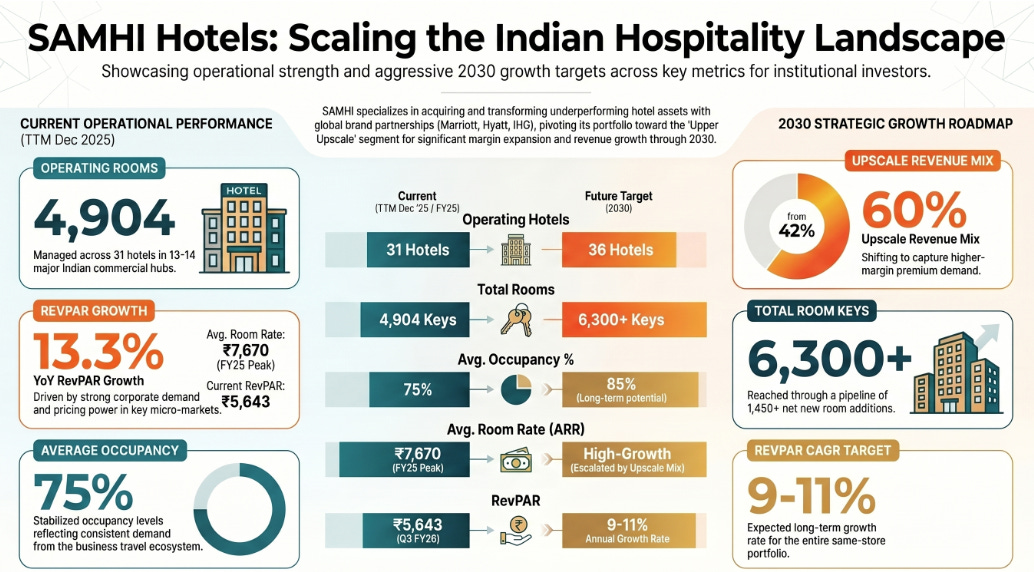

SAHMI is one of India’s largest owners of multi-branded hotel rooms in India with a portfolio of 32 operating hotels and 4,948 keys across 14 key cities. SAMHI’s operating model focuses on acquiring and transforming existing underutilized hotel assets and creating value enhancements through renovation, repositioning and operational improvement. SAMHI’s circle of competence focuses predominantly on business hotels.

Thanks for reading WealthYatra's Newsletter! Subscribe for free to receive new posts and support my work.

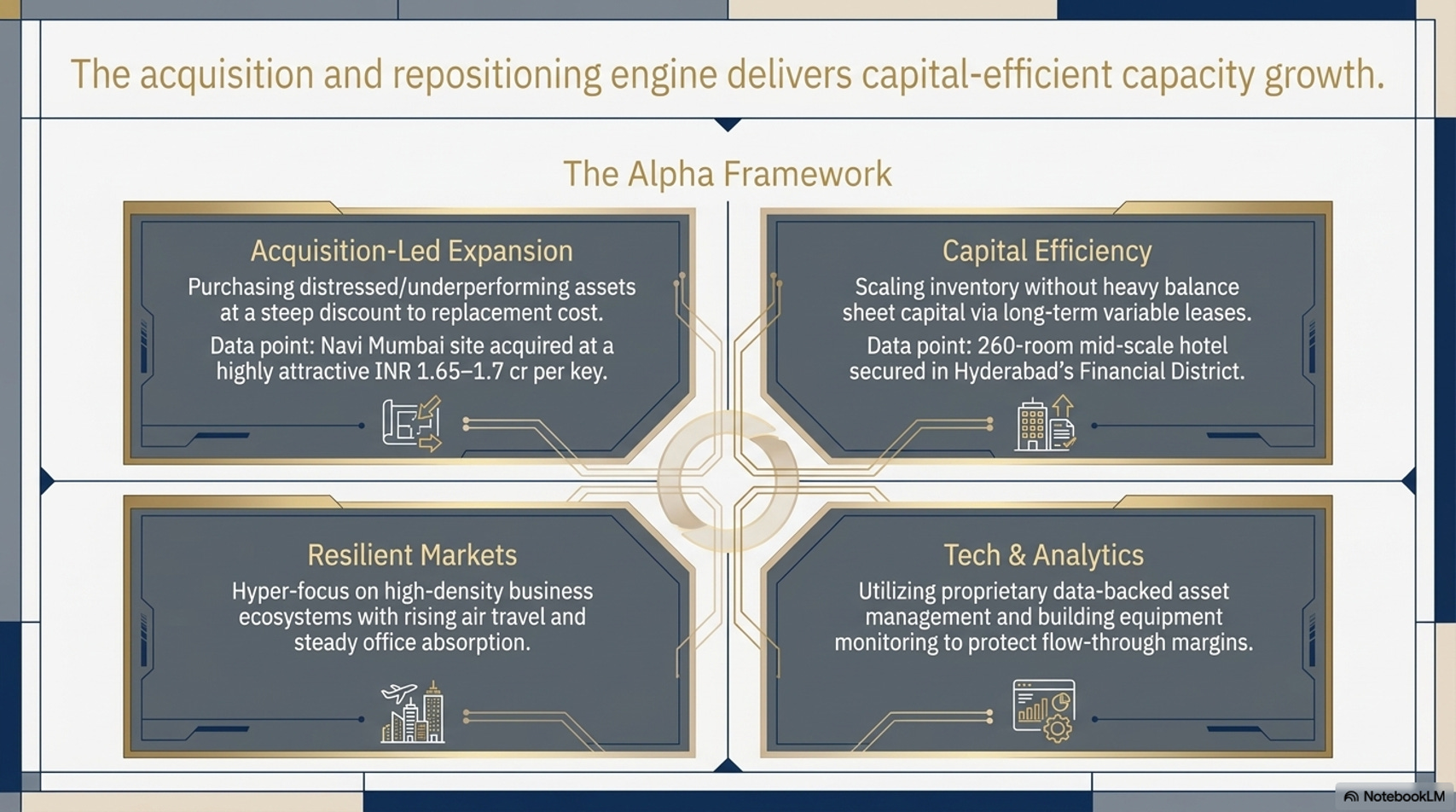

SAMHI Hotels operates an asset-heavy model focused on acquiring, renovating, and owning distressed or underperforming hotels in prime Indian locations. They outsource daily operations to international brands like Marriott and Hyatt, allowing SAMHI to retain 95% of revenue while paying a 4-5% management fee.

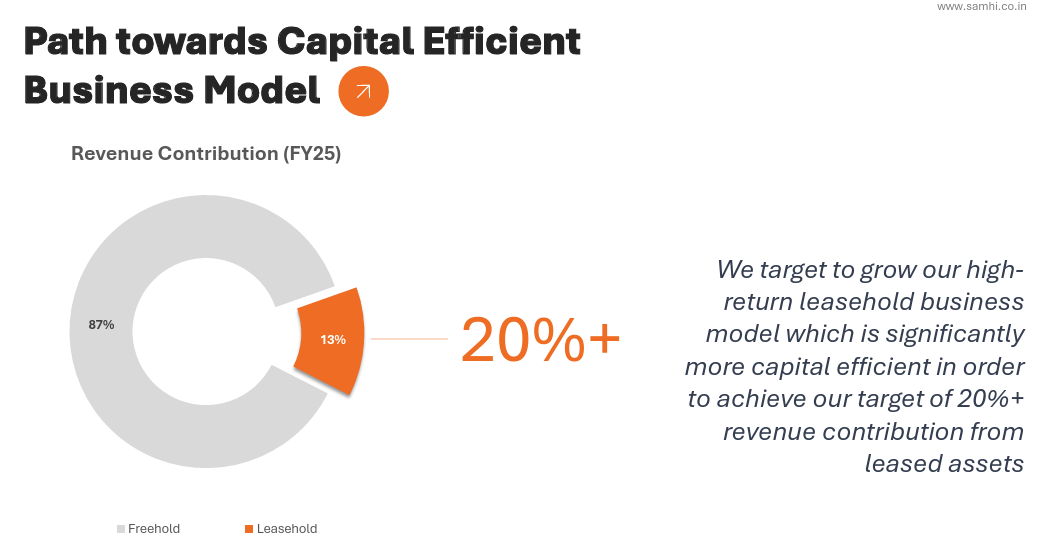

SAMHI uses a hybrid portfolio of freehold (owned) and leasehold (rented) assets, increasingly prioritizing leasehold to boost capital efficiency. In a freehold model, the organization must fund the land, building structure, and approvals, resulting in a capital-intensive development cycle of roughly four years. In contrast, the leasehold model involves the lessor providing the building shell and high-side services, while SAMHI invests only in the fit-outs and operationalization

Segmental Characteristics:

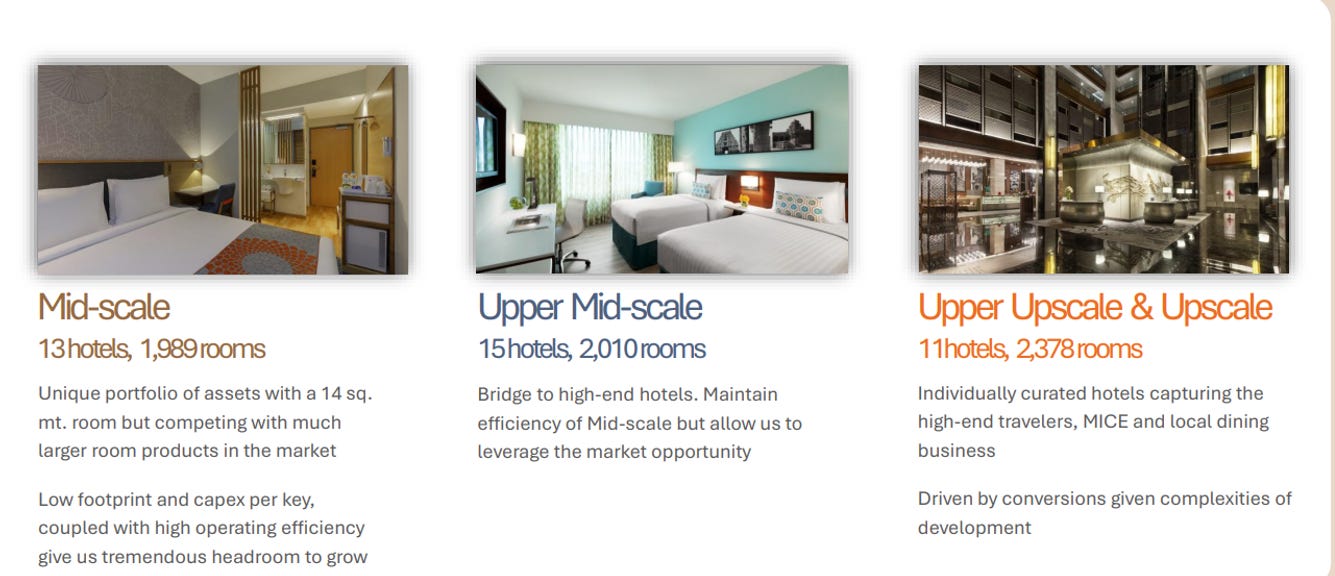

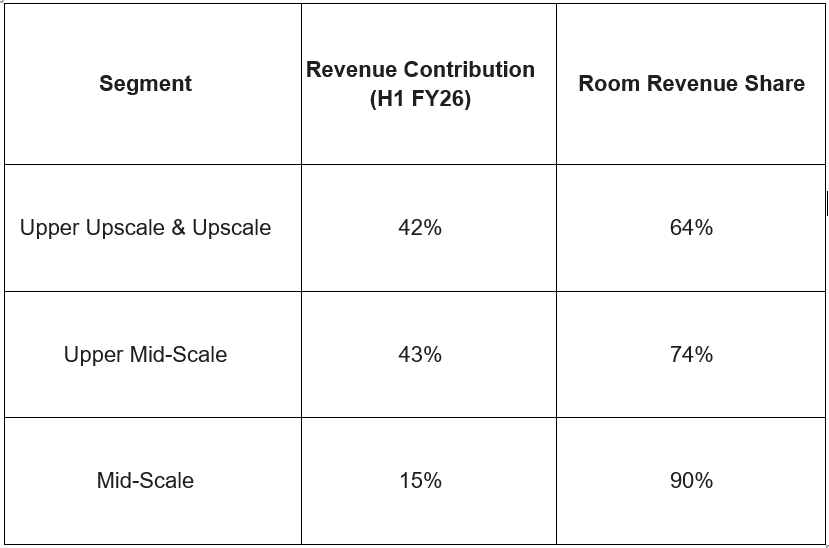

SAMHI’s operational model is built upon three distinct pillars: Upper Upscale and Upscale, Upper Mid-Scale, and Mid-Scale. Each segment serves a specific node in the business travel ecosystem, providing the organization with a natural hedge against volatility in any single price point. The overarching strategy is to maximize the yield of these assets by leveraging the distribution power of international brands while maintaining a lean and centralized operational core.

Key Operational/Financial Metrics:

SAMHI’s consolidated EBITDA margins have demonstrated a strong upward trend, reaching 37.0% in FY2025. At the asset level, the organization achieved a margin of 40.4% for its same-store portfolio. The integration of the ACIC portfolio, acquired in 2023, provides the most compelling evidence of this margin expansion playbook. Within a single fiscal year, the ACIC assets saw their margins rise from 35% to 39% following their conversion to Marriott-managed properties and their integration into SAMHI’s shared service clusters.

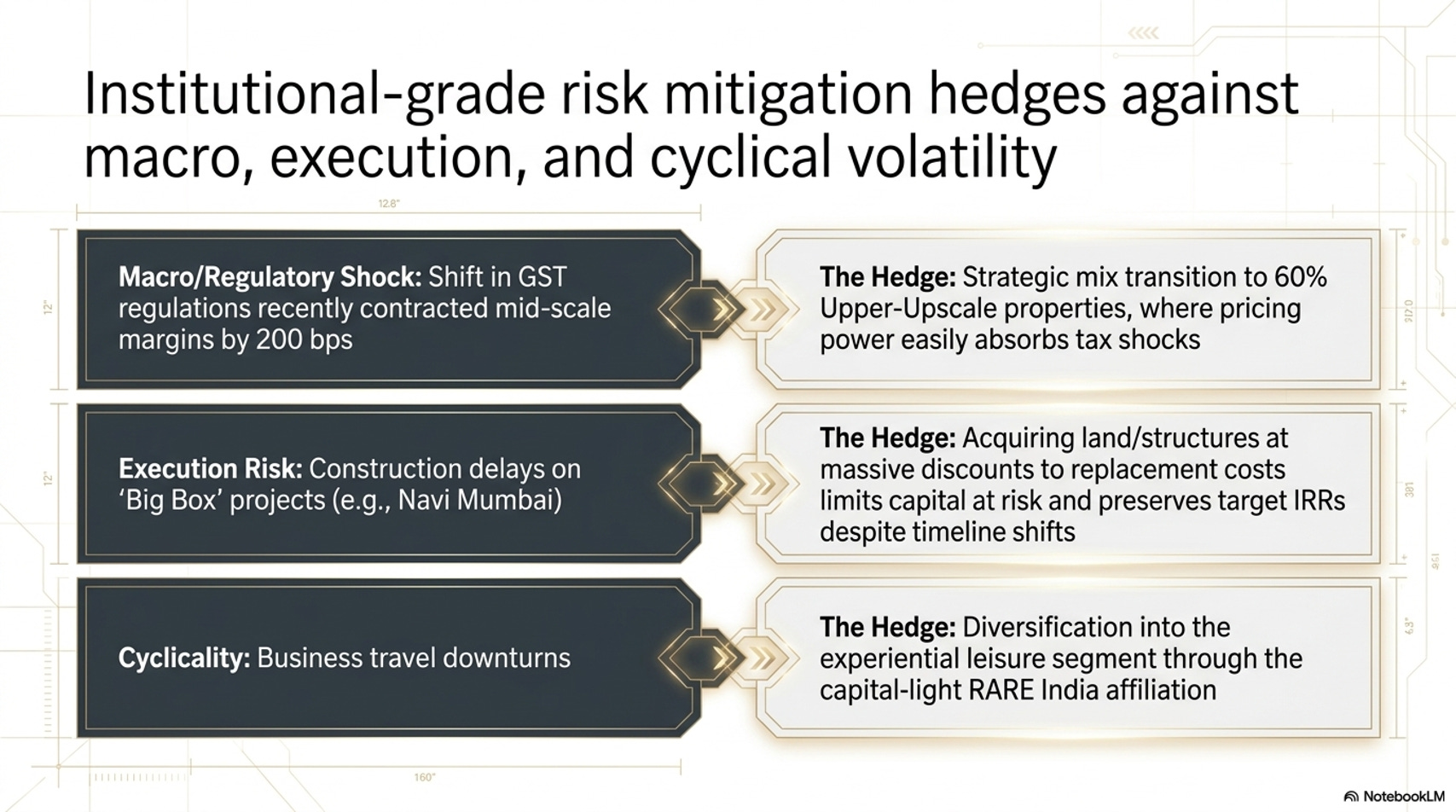

In the third quarter of FY2026, the organization encountered a short-term margin contraction due to shifts in GST regulations. Management views the GST shift as a temporary reporting anomaly and the reduction in tax rates across construction items and the increased affordability for customers will ultimately drive higher occupancy and sales volumes, offsetting the Input Tax Credit loss in the medium-to-long term.

Growth Triggers:

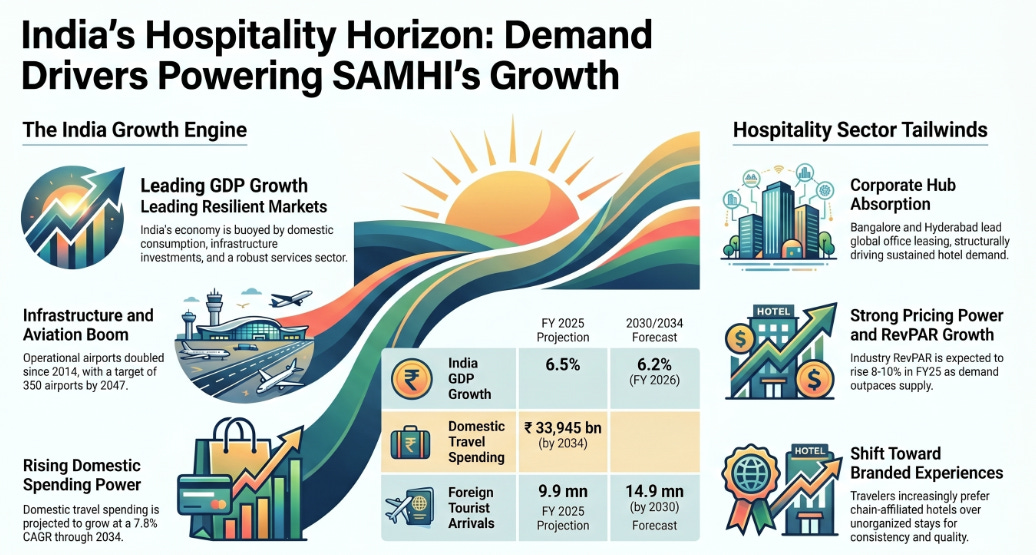

Indian travel has grown considerably with a booming middle class that is increasing becoming a higher spending traveller. Rapid urbanization promoting migration of people from districts & villages to cities aided through growing road connectivity, enhanced rail networks including high-speed rails and a booming aviation traffic. Supply of hotel spaces is unable to match up to the demand requirements. Demand is not restricted to big cities; Tier II and Tier III cities are growing in demand by 13%. Supply growth in such markets is slower at 10%.

The MICE (Meetings, Incentives, Conferences, and Exhibitions Industry) is growing significantly driven by ascending business travel and corporate event planning. The Indian MICE industry is expected to touch $10.52 Bn by the year 2030 with the CAGR of 18% as per Coherent Market Insights. Assuming 10% of this revenue goes to room revenues and F&B in the hospitality sector, it would add ~$330 Mn (Rs 2,739 Cr). This growth is expected to sustain the ARRs of the major players in the hospitality sector.

SAMHI’s Growth plans:

FY 2025 marked a watershed moment for SAMHI, characterized by a fundamental transformation of its balance sheet post IPO and a pivot toward higher-margin upscale assets. The entry of sovereign-linked capital through the GIC partnership and the strategic foray into the experiential leisure segment via RARE India underscore a maturation of the platform’s capital allocation strategy.

The GIC Partnership and RARE India acquisition:

GIC - SAMHI’s strategic alliances with GIC and RARE India represent two different facets of its growth model: the deepening of institutional capital ties for upscale expansion and the foray into the high-margin experiential leisure market.

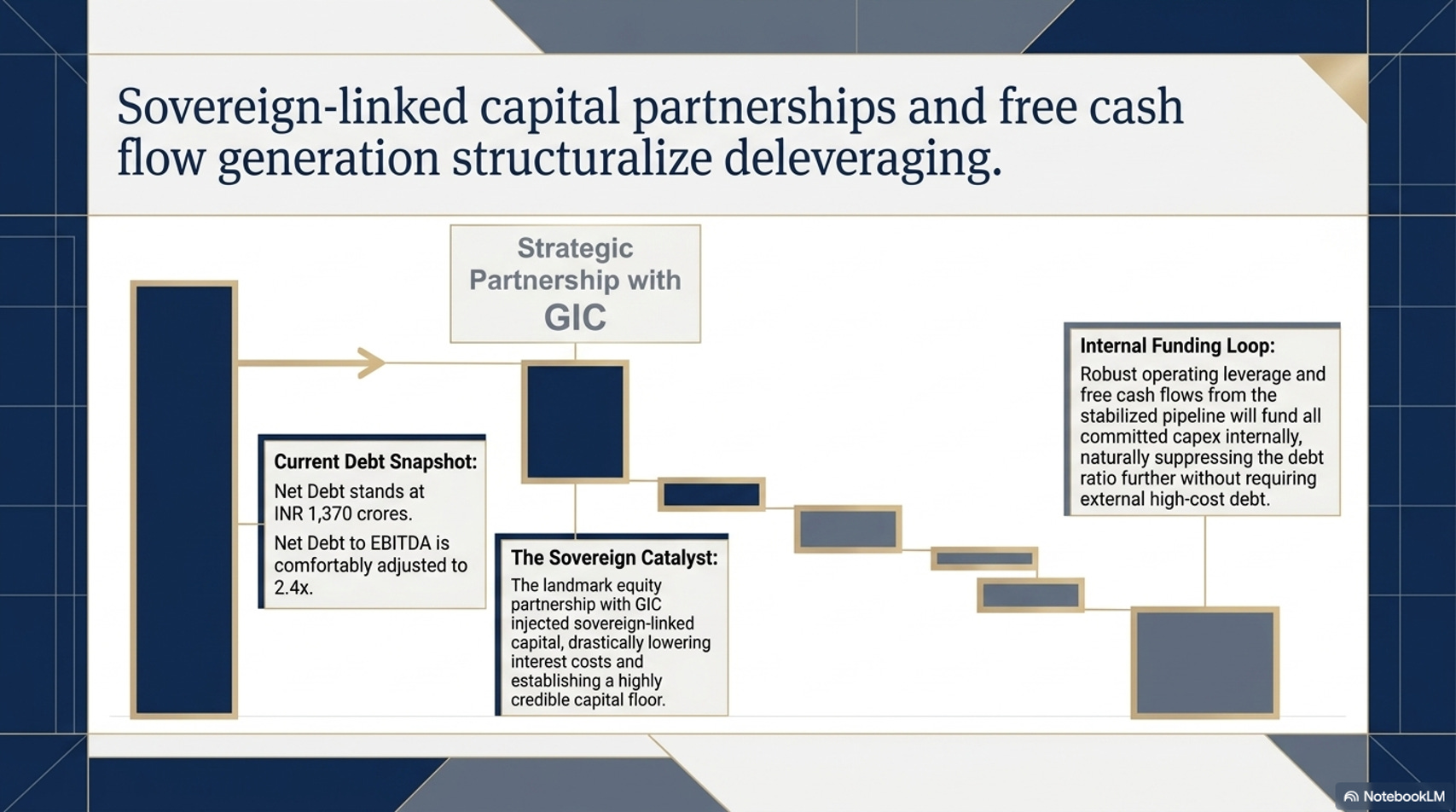

The strategic partnership with GIC involved an investment of ~INR 750 crores into three of SAMHI’s subsidiaries that own key assets in Bangalore and Pune. This partnership was meant to a) strategically benefit a Balance sheet transformation where approximately INR 60 crores of the infusion was deployed toward debt reduction across the SAMHI portfolio, facilitating the rapid drop in leverage seen in FY2026, b) fund capital expenditure of the Westin and Tribute Portfolio dual-branded hotel in Bangalore and c) bring in a sovereign-linked investor like GIC to enhance SAMHI’s credibility with debt markets and provides a stable partner for future “Upper Upscale” acquisitions.

RARE INDIA (Asset Light Expansion Plan) - In early 2026, SAMHI announced the acquisition of a 70% stake in RARE India for approximately INR 47 crores. RARE is a curated platform for boutique, experience-led leisure hotels across India, Nepal, and Bhutan. The deal allows SAMHI to enter the experiential leisure segment—one of the fastest-growing niches in Indian travel—without the capital intensity of asset ownership.

Variable Leases:

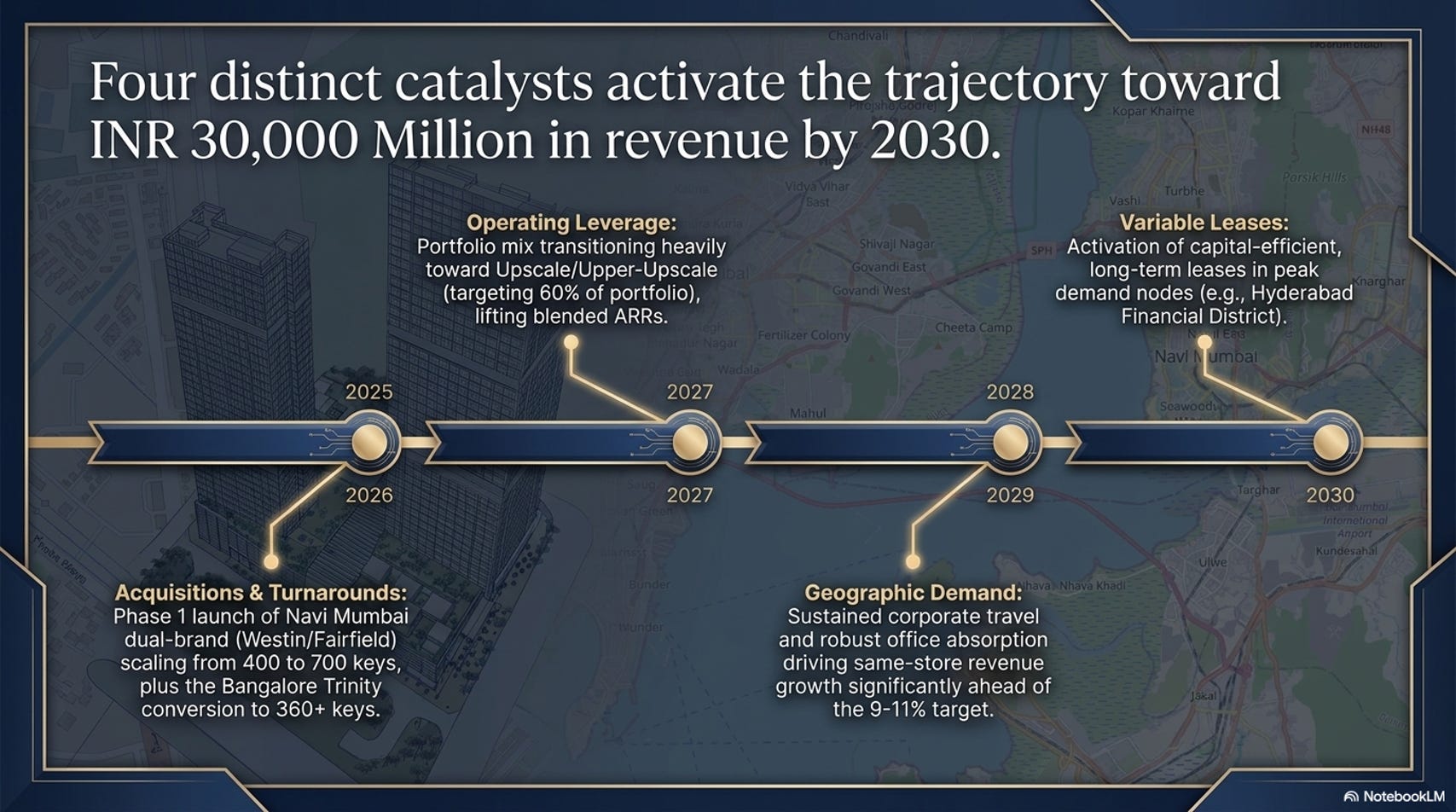

Perhaps the most significant strategic shift in SAMHI’s expansion is the move away from freehold ownership toward long-term variable leases. The implications of this shift for ROCE are profound. Leasehold assets typically deliver returns in the 18% range, compared to 11% for freehold assets, due to the significantly lower capital employed per key. Furthermore, the leasehold model reduces the "lag" between cash outflow and revenue generation, as the construction phase is largely outsourced. SAMHI aims to grow its leasehold revenue contribution from the current 13% to over 20% in the medium term, utilizing this model for high-density business districts like the Hyderabad Financial District.

Big Box Projects and the Rs.3000 crore revenue target by 2030:

SAMHI’s 2030 vision is anchored in a target revenue of INR 3,000 crores, a goal that requires the organization to roughly triple its current top line. This growth is not speculative; it is supported by a committed pipeline of “Big Box” assets that will add massive room inventory in India’s deepest commercial markets.

Navi Mumbai: The Entry into India’s Financial Capital - The most significant growth project announced post-IPO is the dual-branded Westin and Fairfield development in Navi Mumbai. This project is strategic due to its proximity to the upcoming Navi Mumbai International Airport, the Atal Setu (MTHL), and the burgeoning data center and commercial developments in the region. The cost per key for this project is highly attractive at INR 1.65-1.7 crores, which is a significant discount to the replacement cost of similar upscale developments in the Mumbai Metropolitan Region.By securing this site through the ACIC acquisition (where the land was valued at a deep discount), SAMHI has created a high-conviction growth engine that will materially contribute to its 2030 revenue targets.

Hyderabad and the Financial District Play: Hyderabad has emerged as one of SAMHI’s strongest performing markets. The organization is expanding its footprint in the Financial District by securing a 260-room mid-scale hotel under a long-term variable lease.This property, combined with the existing Sheraton and Fairfield properties, gives SAMHI a unique dominance across all three price points in a precinct where tech giants like Google and Amazon are expanding aggressively. Furthermore, the W Hyderabad in HITEC City—a 170-room luxury lifestyle hotel—is targeted for a December 2026 opening.As a “marquee” asset, the W is expected to command the highest ARRs in the SAMHI portfolio, serving as a catalyst for the organization’s upscale transformation.

Bangalore and the Whitefield Transformation: In Bangalore Whitefield, SAMHI is executing a transformational expansion of the Trinity Hotel (acquired in 2024). The property is being renovated and expanded into a 360+ room dual-branded hotel under the Westin and Tribute Portfolio brands. By increasing the inventory and repositioning the brand, SAMHI expects to drive a 50% growth in revenue for this specific asset, with ARRs already trending toward INR 10,000 post-Marriott management.

Data driven Productivity/Operational Excellence:

Operational excellence is underpinned by “SiD” – SAHMI’s inhouse and proprietary asset management tool. This tool allows the management team to monitor performance indicators—such as weekday vs. weekend occupancy trends and revenue contribution from specific IT clusters—on a granular, day-by-day basis. By integrating financial and operational data, SiD enables “predictive” asset management, allowing the organization to identify underperforming cost lines or missed revenue opportunities in real time. This technological edge is a key driver of the margin improvements and ROCE expansion seen in the mature portfolio.

Labor Management:

The hospitality sector in India faces a chronic shortage of skilled labor, which can hamper service standards and drive-up wages. SAMHI addresses this through its Bespoke Management Development Program (MDP) in partnership with the Indian School of Hospitality (ISH). By investing in talent development and maintaining a centralized HR and payroll cluster, the organization plans to keep its total payroll expense at approximately 16% of revenue, significantly lower than the industry average for full-service hotels.

Key Factors to watch:

The hotel stocks have underperformed recently due to the geopolitical climate and the recent travel disruptions from India’s largest airliner. SAMHI’s performance was no exception.

The larger investment community is focussed on 3 important parameters for a potential re rating. SAMHI’s adherence to these factors could turn the tide in its favor.

Deleveraging Roadmap and Net Debt Reduction: As of September 2025, SAMHI’s net debt-to-EBITDA ratio reached 2.9x, a significant improvement from the 8.7x recorded in FY2023. The total net debt stood at INR 1,370 crores in H1 FY2026, but the organization has set a clear goal of reducing debt by a further INR 300 crores through internal cash flows by 2030.

SAMHI’s roadmap for debt reduction is supported by three primary pillars:

a) Investible Surplus: The organization expects to generate over INR 900 crores in investible surplus over the next five years, assuming a 13-15% revenue CAGR. This surplus is calculated after fulfilling all committed capex, interest payments, and mandatory debt repayments.

b) Asset Recycling: SAMHI has demonstrated a willingness to recycle capital by selling non-core or “unbranded” assets. The organization has a total target of INR 200 crores from such initiatives.

c) Refinancing and Maturity Profiling: The average tenure of SAMHI’s debt facilities is approximately 12 years, with over 75% of the principal amortization scheduled after the seventh year. This “back-ended” repayment structure allows the organization to allocate current cash flows toward growth projects during the upcycle, ensuring that liquidity is preserved for value-accretive initiatives.

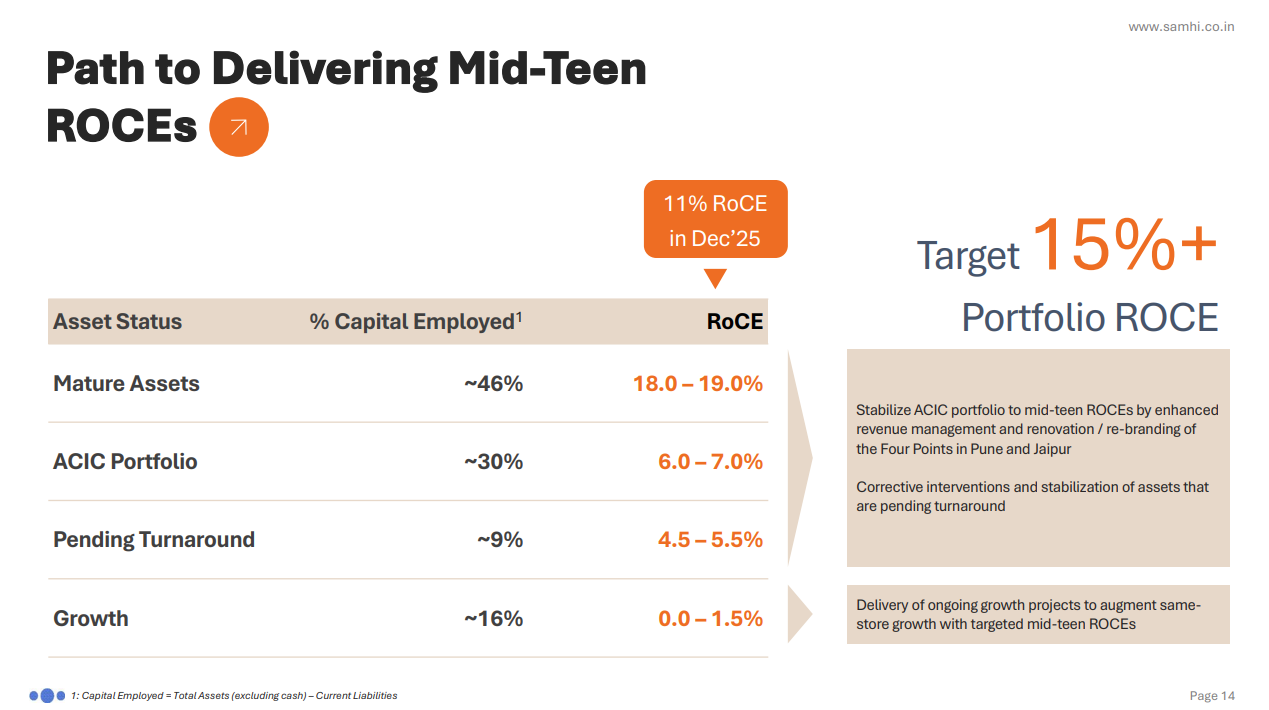

ROCE Enhancement:

For institutional investors, the most critical metric in the SAMHI story is the Return on Capital Employed (ROCE). The organization has established a clear trajectory to move its portfolio-wide ROCE from the current 10-11% range to a target of over 15%. This improvement is predicated on the transition of “Growth” and “Turnaround” assets into “Mature” assets, alongside an increased reliance on capital-efficient leasehold structures.

Execution: SAMHI’s management team has strong domain expertise, successful project implementation, management capabilities and long-standing global relationships in the hotel industry but the crux of the rerating remains with the management’s capability to execute its plans.

Risks/Ant- Thesis:

Other than the risks mentioned in the slide, here are few issues that may be issues to consider in SAMHI’s journey.

The GIC deal necessitates a 65-35 joint venture ratio that may complicate future exit strategies for individual assets. While the platform allows for scale, GIC partnership relates to the complexity of shared ownership.

The transition of RARE from a B2B representation platform into a B2C brand involves significant execution risk. Management acknowledged that not all properties currently under the RARE umbrella may transition to the Marriott platform, especially if they have conflicting affiliations.

As mentioned earlier, management’s efficiency in execution for their stated targets is critical. Any changes in key management positions may pose significant risk to the rerating chances.

Valuations:

SAMHI’s current EV/EBITDA (approx. 11 times) currently is the lowest amongst the peers in the Hospitality sector in India. While Chalet Hotels and Juniper Hotels are predominantly comparable to SAMHI in their operating model, other listed hotels that utilize a managed or hybrid model (combining owned and managed assets) and focused on reducing capital intensity through third-party management or partnering with global brands enjoy higher multiples.

There is no specific guidance from management on future revenue growth other than the Rs 3000 crore target by FY30, other than an assumption of 9 to 11% CAGR in same store revenue. With SAMHI clocking a 9M revenue for FY 25-26 of Rs 903 crores, one can make a reasonable assumption for them to end up FY25-26 revenue at approx. Rs 1250-1300 crores. The FY30 target therefore assumes an approx. CAGR of 24% which implies that management expects significant growth from their big box projects with the operational leverage playing out from FY27-30.

Given their pipeline of 1900 rooms under development with a focus on upscale and upper-upscale projects, one can expect to see a revenue shift towards higher-margin upscale segments improving quality of long-term earnings.

Even at conservative 12% growth rate and a 35% EBITDA due to the focus given the expected focus on the Upper Upscale and Upscale segment whose contribution is expected to reach 60% of total revenue, FY 27-28 revenue would approx. touch Rs 1630 crore. Expected EBITDA would therefore be around 575 crores. Given the focus initiatives on big box projects, ROCE improvements including deleveraging, one can probably assume a slightly higher EV/EBITDA multiple, but at a conservative 12 times multiple, expected market cap would be 6900 which is almost a 2x from the current market cap of Rs 3660 crores. If SAMHI’s management is able to match its guidance, the rerating from the current level would be significant.

Summary:

The “SAMHI Playbook”—acquiring underperforming assets at a discount and transforming them through global brand partnerships and data-led management—is now operating at scale. While short-term challenges such as GST adjustments and labor shortages persist, operational leverage play out with increasing ROCEs, deleveraging, long-term structural drivers of office leasing, infrastructure investment, and rising disposable incomes remain overwhelmingly positive. For investors, SAMHI offers a high-conviction play on the modernization of the Indian services economy, supported by a management team that has demonstrated an ability to execute turnarounds even in the most volatile conditions.

Information cited in this blog are from investor presentations, annual reports, credit reports and other publicly available information. The content provided is for informational and educational purposes only and not personalized financial, investment, or trading advice.