Overview:

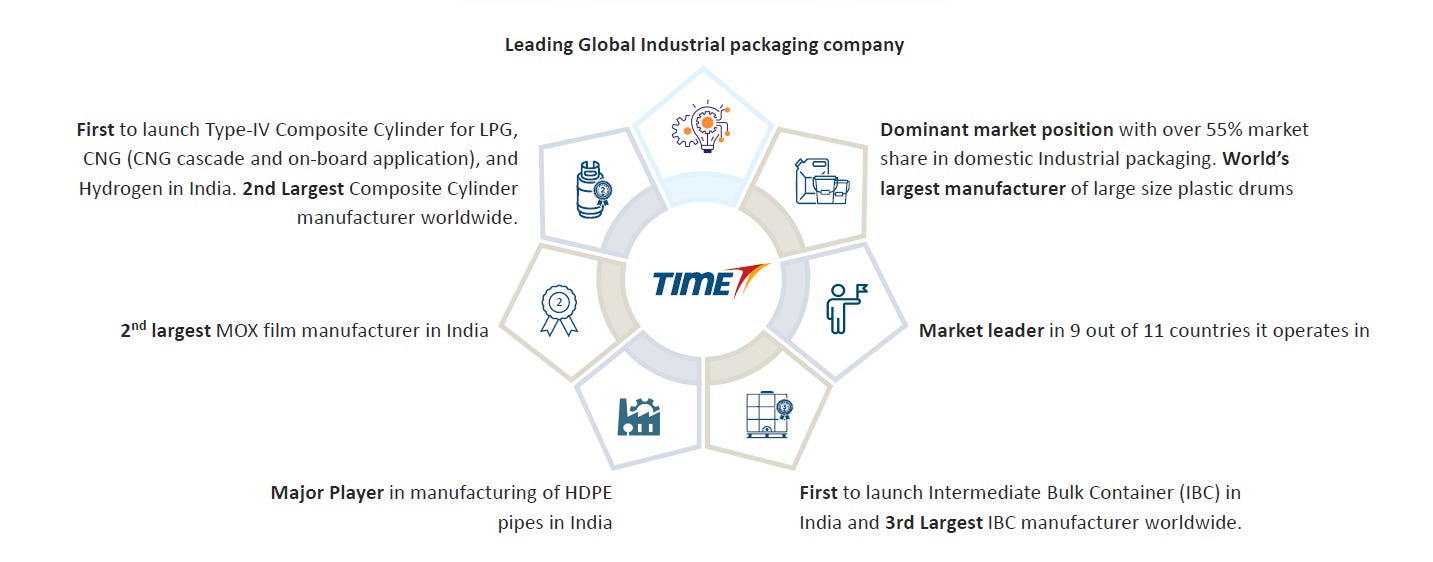

Time Technoplast Ltd. (“TTL”) is a multinational conglomerate with a robust presence in 11 countries and an industry leader in the manufacturing of polymer products. Established in 1989, TTL’s business is characterized by the legacy cash-generative engine of industrial packaging and the high-growth, high-margin frontier of composite pressure vessels and clean energy storage.

Product Portfolio:

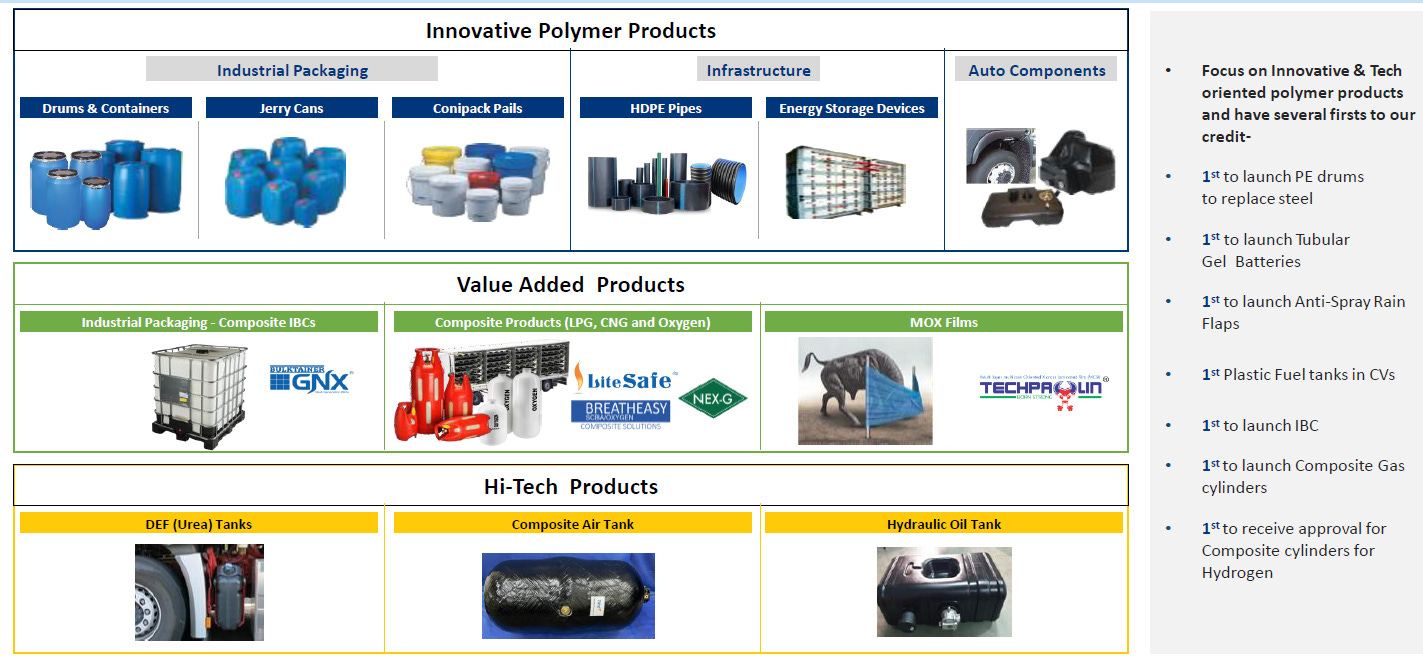

The company’s portfolio is broadly categorized into Polymer Products and Composite Products, serving industry segments such as industrial packaging, infrastructure, automotive, and high-tech energy storage.

Industrial Packaging: The Core Revenue Engine

The industrial packaging segment serves as TTL’s “bread-and-butter,” contributing approximately 73-75% of total consolidated revenue.

● Polymer Drums and Containers: TTL is the world’s largest manufacturer of large-size plastic drums. The shift from steel drums to polymer drums is a secular trend driven by the latter’s superior corrosion resistance, lighter weight, and lower total cost of ownership.

● Intermediate Bulk Containers (IBC): TTL was the first to launch IBCs in India and is now the 3rd largest manufacturer globally. These containers, provide significant space-saving advantages and bulk handling efficiencies for chemical and food processing giants.

● Jerry Cans and Pails: These cater to the FMCG and construction chemical sectors, where precision in dispensing and spill-proof integrity are paramount

Infrastructure and Lifestyle Solutions:

TTL utilizes its polymer expertise to address large-scale infrastructure projects and consumer applications.

● PE Pipes: The company is a major player in the manufacturing of High-Density Polyethylene (HDPE) and Double Wall Corrugated (DWC) pipes in India critical for water management, sewage systems, and the government’s ambitious “Smart Cities” and “Nal se Jal” initiatives.

● Technical and Lifestyle Products: This includes specialized products like turf and matting (Duro brand), disposable bins, and automotive rain flaps. The automotive sub-segment also produces plastic fuel tanks for commercial vehicles, another area where polymer is replacing metal due to weight reduction requirements

Value-Added Products (VAP): The Growth Frontier

The VAP segment, comprising IBCs, composite cylinders, and MOX films, represents the future of TTL’s margin expansion strategy.

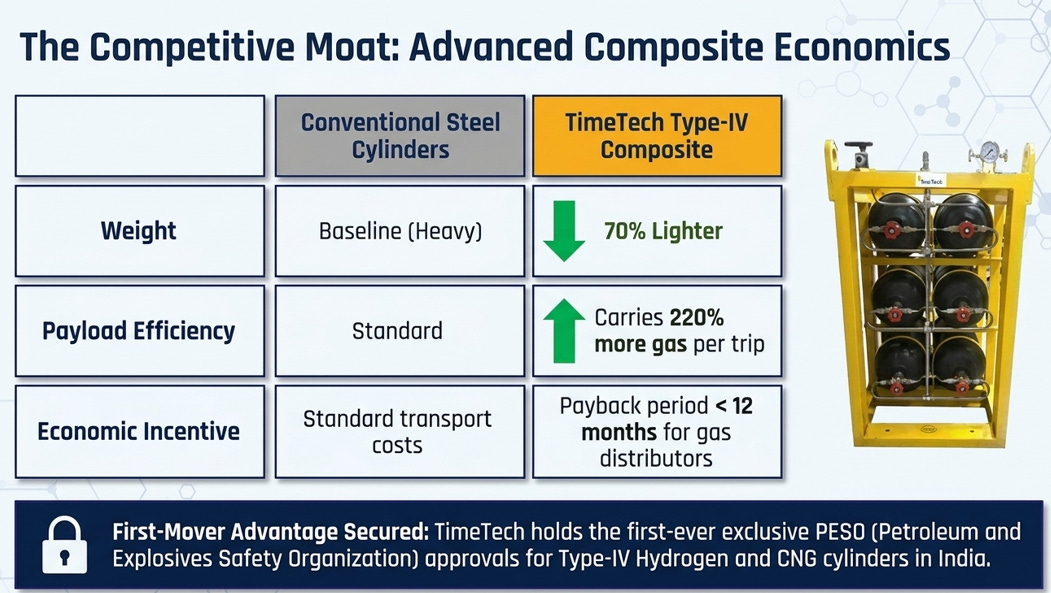

● Composite LPG Cylinders: These are 70% lighter than traditional steel cylinders and offer explosion-proof safety features. TTL is currently supplying 10kg cylinders and has submitted designs for 14.2kg cylinders to domestic Public Sector Oil Marketing Companies (PSU OMCs).

● Type-IV CNG Cylinders: These carbon-wrapped, metal-free vessels are used in CNG cascades for gas transportation from mother stations to daughter stations. They offer 2.2x more gas carrying capacity per trip compared to steel, leading to a payback period of less than 12 months for gas distributors.

● MOX Films (Techpaulin): TTL is the 2nd largest manufacturer of these multilayer, multi-axial oriented cross-laminated films in India. MOX films provide superior strength-to-weight ratios and are essential for industrial waterproofing, agricultural covers, and protective gear.

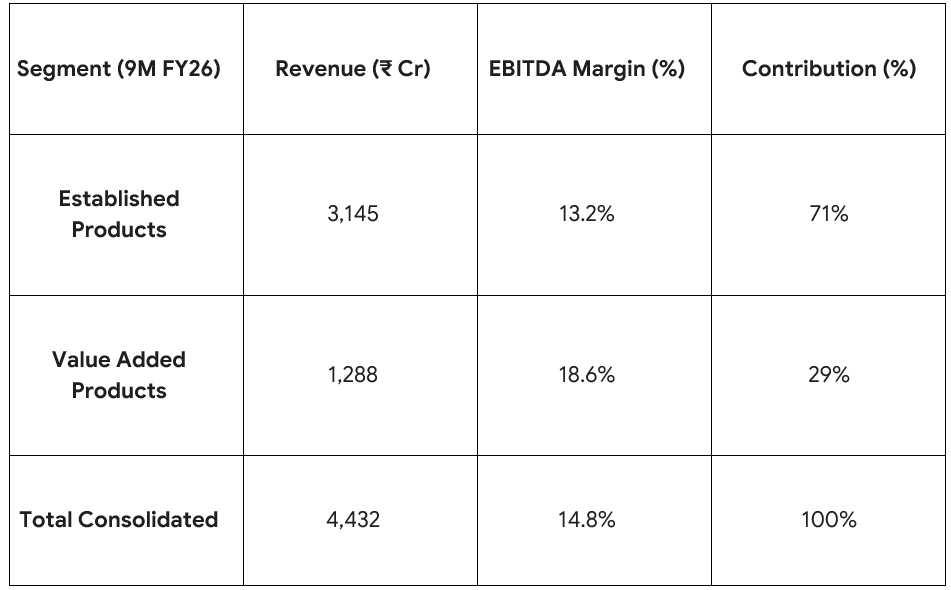

Segmental Analysis and Margin dynamics:

TTL’s financial performance is increasingly driven by its transition toward a more profitable product mix. The management’s focus on increasing the share of Value-Added Products (VAP) is the primary lever for consolidated EBITDA margin expansion.

Established vs. VAP comparsion (9MFY26)

The data indicates that while established products provide the scale and a steady EBITDA margin of ~13.2%, the VAP segment is the high-octane growth engine, yielding margins of 18.6%. highlighting the accelerating shift in business composition.

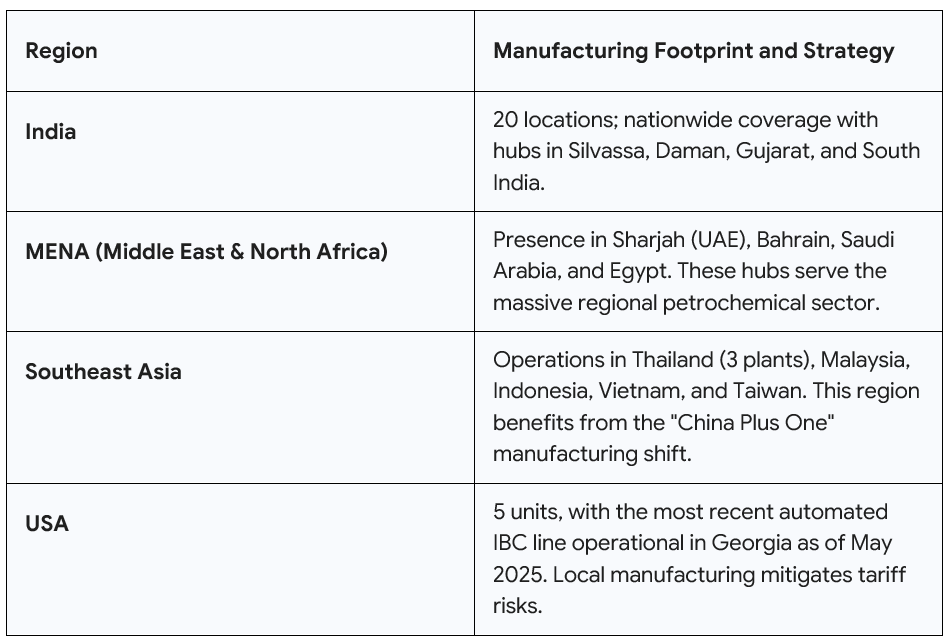

Geographical footprint:

TTL’s operational philosophy works on the principle of maintaining its manufacturing units in proximity to chemical and industrial hubs to remain cost-competitive since industrial packaging is freight-intensive.

● India: Contributes 64% of total revenue with an EBITDA margin of 15.0%. The domestic market is fuelled by infrastructure spending and the burgeoning clean energy transition.

● Overseas: Contributes 36% of revenue with an EBITDA margin of 14.5%. The overseas segment is primarily industrial packaging-centric, with high growth observed in the US and Southeast Asian markets.

Growth Triggers, Industry trends and Moats:

The composite packaging market is experiencing rapid growth, valued at $13.74 billion in 2025 and projected to grow at a CAGR of 13.49% to reach $37.82 billion by 2033. Driven by the need for lightweight, durable, and sustainable solutions, growth is accelerating in industrial applications, specifically through advanced polymer composites, multi-layer films, and high-strength, low-waste materials.

The convergence of global environmental mandates and India’s infrastructure modernization is creating significant growth triggers for TTL’s product lines.

1. The “Type-IV” Revolution in Gas Transportation:

The shift from steel to composite cascades is perhaps the most significant growth trigger for the next five years.

CNG Cascade Potential: India is witnessing a rapid expansion of CNG refueling stations. TTL’s composite cascades are 50% lighter and carry 2.2x more gas per trip than steel, significantly reducing the carbon footprint of transportation.

CBG and Bio-Gas: The expansion of Compressed Bio-Gas (CBG) under the SATAT scheme presents a ₹2,000 Cr per year market opportunity for composite storage solutions.

Replacement Cycle: The domestic LPG market in India has an installed base of 360 million steel cylinders, with 25 million requiring replacement annually. TTL aims to capture a significant portion of this ₹6,000-8,000 Cr replacement market as consumers and OMCs prioritize safety and weight reduction.

Hydrgen economy: Future-ready storage:

As India pushes toward becoming a global hub for Green Hydrogen, TTL is the early leader in high-pressure hydrogen storage.

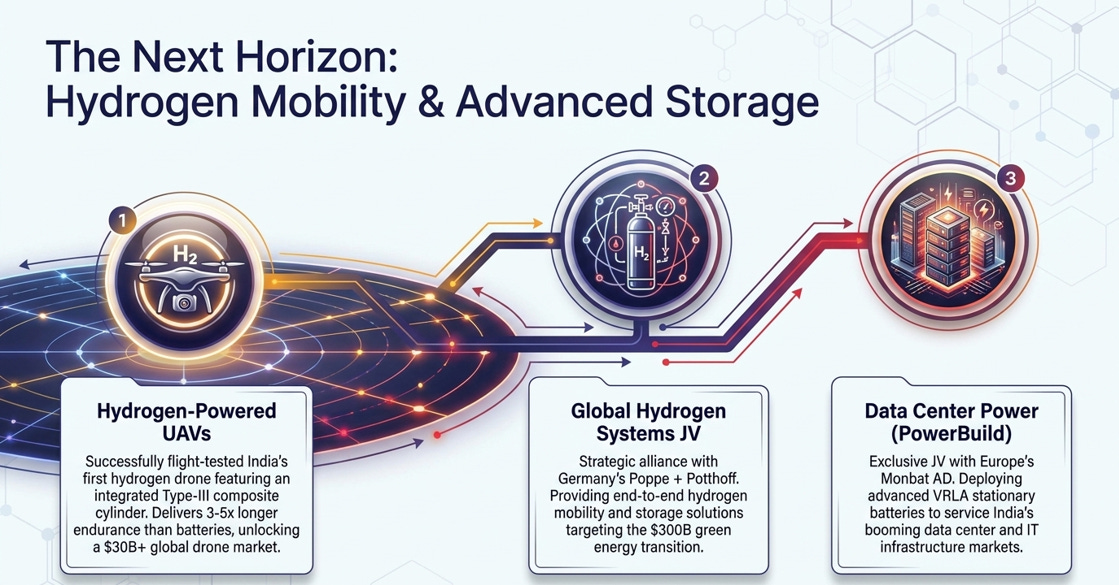

Mobility Applications: TTL has developed Type-IV carbon-wrapped cylinders for hydrogen-powered cars and buses, which offer a 90% weight reduction compared to metal.

Drone Ecosystem: TTL successfully developed India’s first hydrogen-powered drone with an integrated Type-III composite cylinder. This drone offers 3-5x the endurance of battery-powered drones, making it ideal for mapping and long-duration surveillance in the $30B global drone market.

Earlier in this week, TTL obtained Hydrogen Cylinder approval for use in Buses, Trucks and Trailers from PESO.

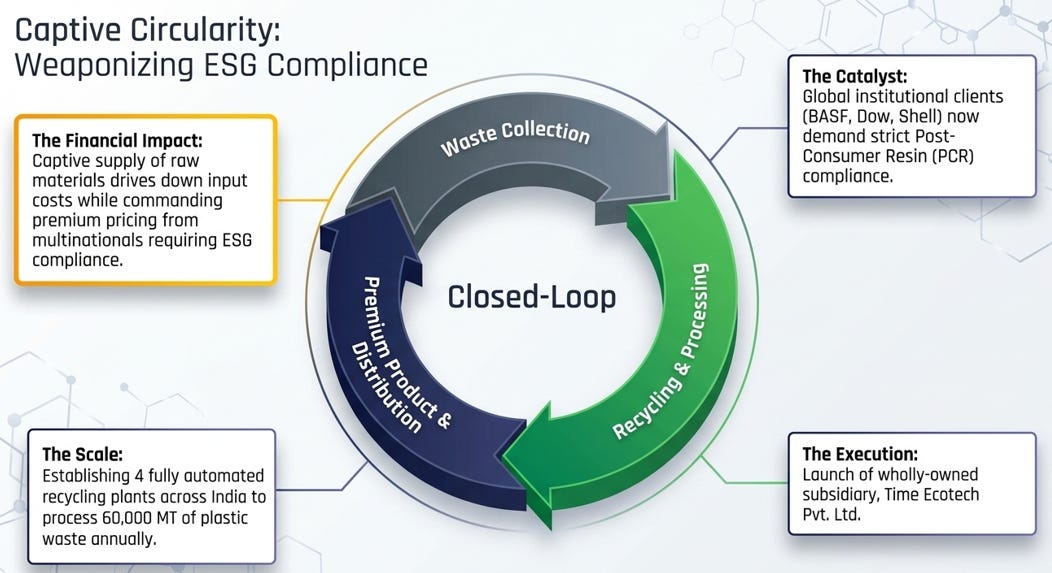

Sustainability and Circular Economy:

Time Ecotech: TTL is setting up three recycling facilities in India with a 12,000 MT annual capacity for captive consumption. This ensures a steady supply of recycled raw materials, supporting PCR compliance for TTL’s global institutional clients who have pledged to meet aggressive ESG targets.

Technological and Regulatory Moats:

PESO Exclusivity: TTL is currently the only company in India to receive PESO approval for Type-IV high-pressure composite cylinders for Hydrogen and CNG cascades. These approvals involve rigorous validation cycles that act as a massive barrier to entry for domestic competitors.

Vertical Integration: TTL produces its own HDPE liners and manages the entire carbon-fiber wrapping and filament winding process in-house. This vertical integration allows for superior cost control and quality consistency.

Proprietary Multi-Layer Tech: TTL holds an extensive patent portfolio covering multi-layer films and blow-moulding processes, enabling it to offer superior barrier properties compared to standard plastic containers.

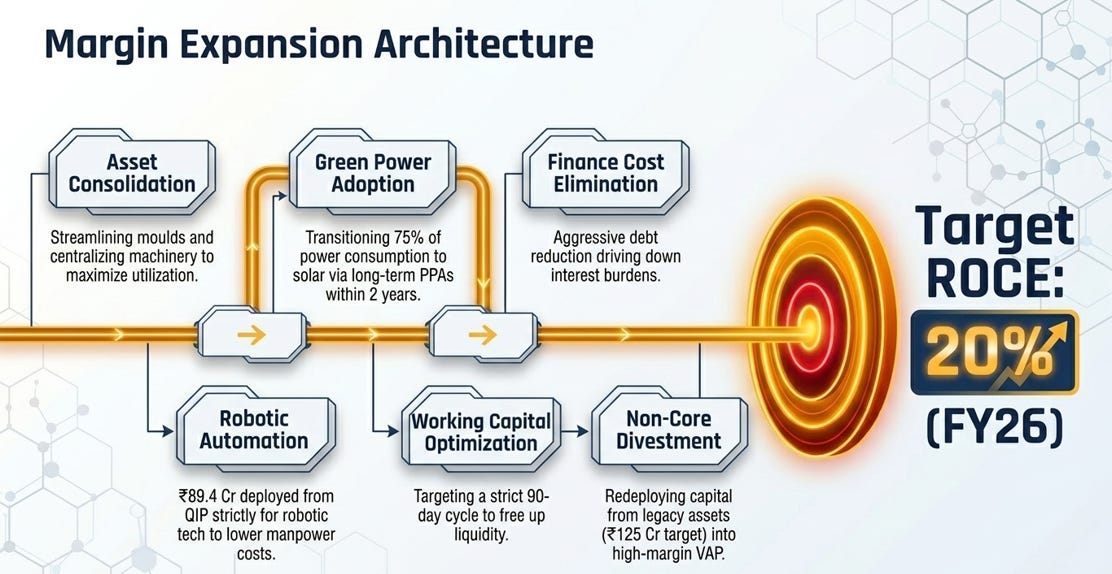

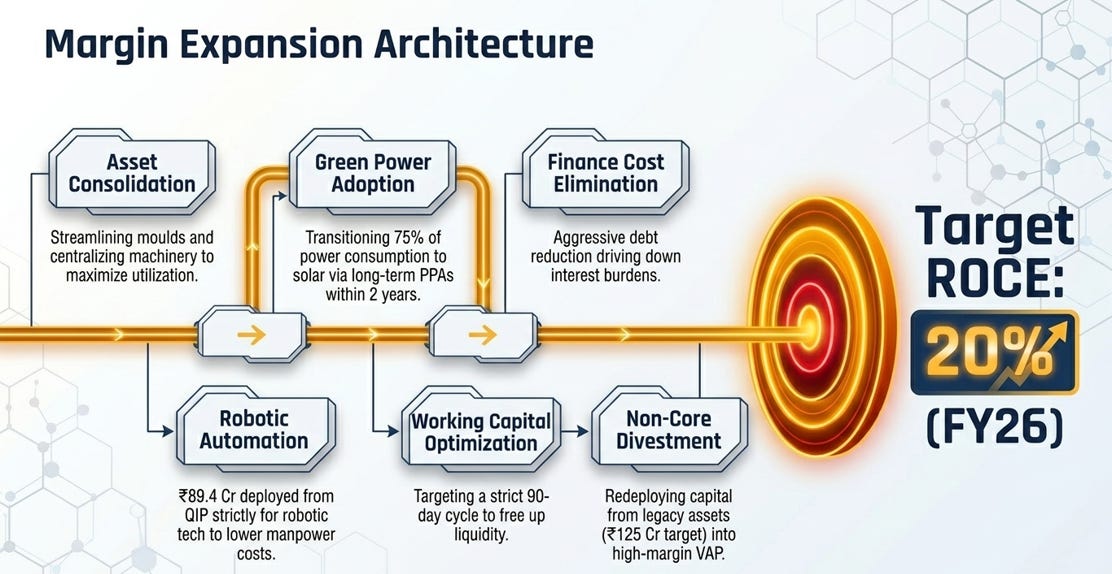

Strategic Growth Initiatives and Financial Roadmap:

TTL is currently executing “Project Vistriaa,” a comprehensive strategic initiative aimed at de-leveraging the balance sheet and funding high-margin expansion.

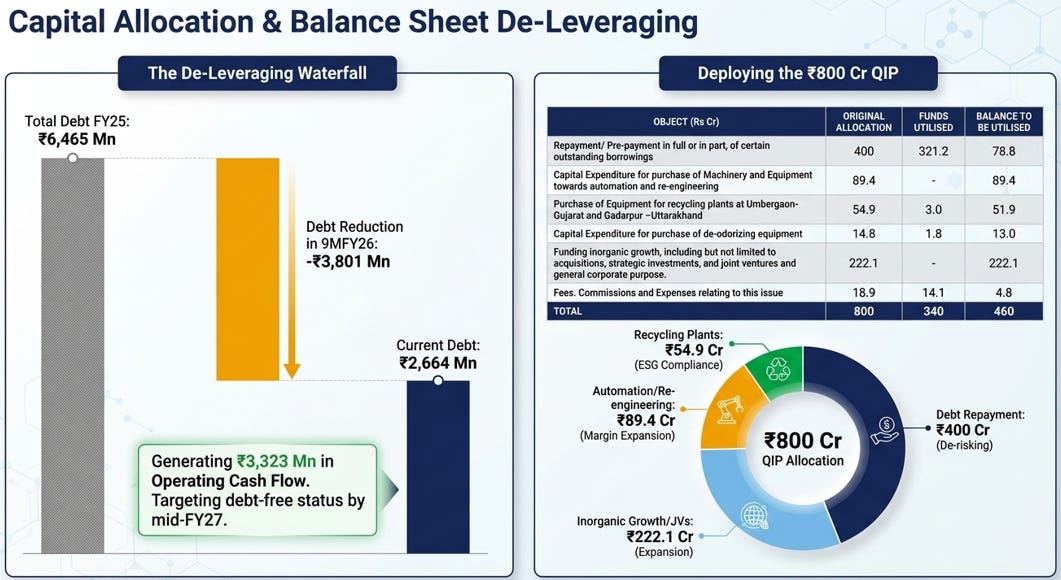

Qualified Institutional Placement (QIP): In November 2025, TTL raised ₹800 Cr through a QIP, issuing shares at ₹201.12 per share. Bulk of this QIP was meant for borrowing repayment and funding strategic acquisitions while the remaining proceeds were meant for automation & re-engineering, recycling plants and de-odorizing equipments.

Inorganic growth and synergies: TTL is in the process of acquiring Ebullient Packaging, an unlisted FIBC (Flexible Intermediate Bulk Container) manufacturer with an annual turnover of ~₹250 Cr. This acquisition will allow TTL to offer a comprehensive “one-stop shop” for industrial packaging, combining rigid drums and IBCs with flexible solutions.

Debt Reduction and Finance Costs: TTL has utilized a substantial portion of QIP proceeds to pare down high-interest borrowings.

Debt Trajectory: Total debt was reduced by ₹380 Cr in 9M FY26, bringing the total debt down to ₹266 Cr as of December 31, 2025, compared to ₹646 Cr in FY25.

Debt-Free Target: Management has provided “very clear visibility” to becoming a completely debt-free company within the next six months (by mid-FY27).

Interest Savings: Annualized finance costs, which were historically around ₹100 Cr, are expected to fall to ₹25-30 Cr, which will primarily represent documentation and non-fund-based facility charges.

Return on Capital (ROCE) Targets:

TTL has a history of disciplined ROCE improvement, moving from 14% to 18% over the last four years. As of 9M FY26, the company achieved 18.6% against a FY26 target of 20%

Long-Term Goal: o Management targets 22-26% ROCE by FY28, driven by higher asset utilization (Sales/Gross Block moving from 1.6x to 2.1x) and the ramp-up of the VAP segment.

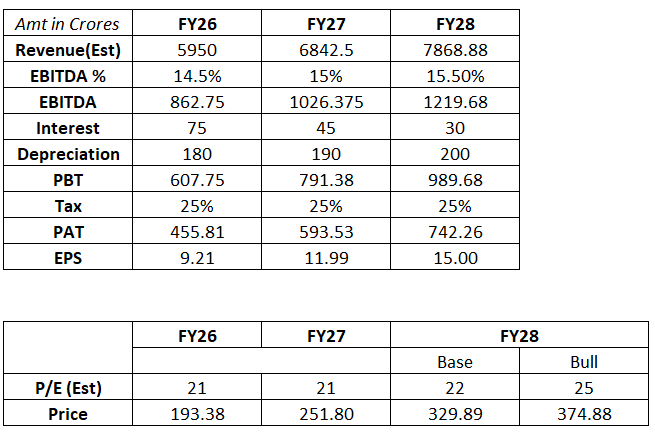

Forward Looking Valuations:

TTL is currently trading at a P/E multiple that is significantly lower than its industrial peers like Supreme Industries, despite having a superior growth profile in the clean energy segment. With enough tailwinds in the sector, being a market leader supported by innovation assisting VAP mix expansion and the company achieves net-cash status, a re-rating is imminent in the near term. The table below assumes a 15% revenue growth while cautiously increase its EBITDA % given its increased concentration in VAP.

The base case assumes TTL continues its steady growth in packaging while successfully ramping up its CNG cascade business to meet current station expansion targets while the bull case factors in an acceleration of the Hydrogen drone market and a breakthrough order from OMCs for 14.2kg composite LPG cylinders.

Promoters of TTL have been actively increasing their stake of late, with recent open market purchases by entities like Time Exports Private Limited and Time Securities Services Private Limited. These actions, such as acquiring 1.44 lakh shares at ~₹198, signal confidence in the company’s growth by the promoters.

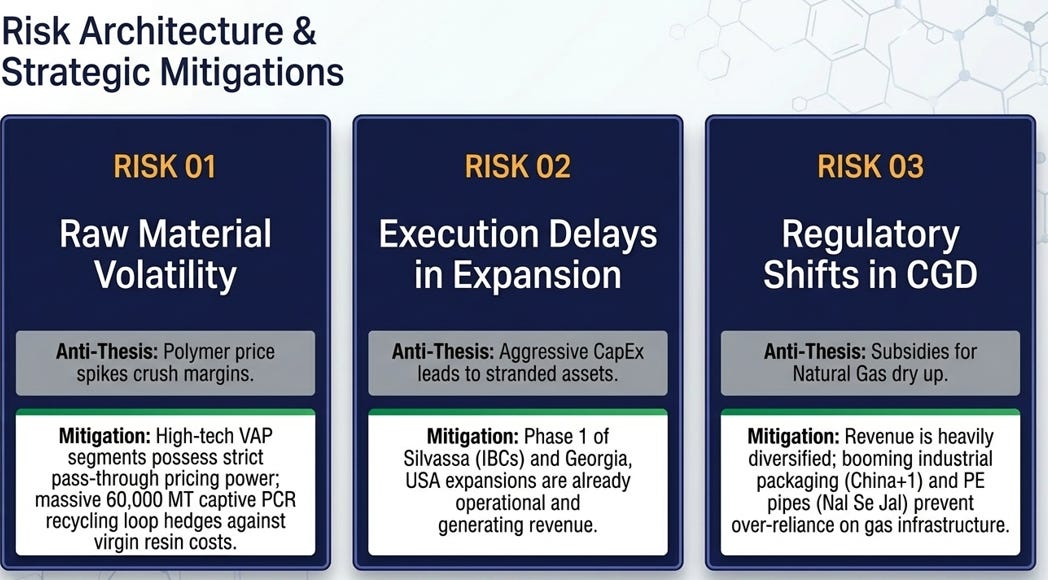

Risk/Anti-thesis:

Summary:

TTL is uniquely positioned with its mastery of polymer engineering serving a formidable “moat” in industrial packaging and a self-sustaining cash generator for its high-tech composite ambitions. The successful execution of “Project Vistriaa” and the subsequent QIP fund raise has helped in paring down debt, focusing capital on automation and clearing the path for significant expansion in ROCE and EPS through Time Ecotech recycling initiative The upcoming commercialization of composite fire extinguishers and 250L CNG cylinders, alongside the pilot-stage hydrogen drone applications, provides a long-term growth visibility.

While investors must remain cognizant of raw material price sensitivities and the pace of regulatory approvals, the risk-reward profile for TTL remains highly attractive. As VAP mix rises toward the 35% target, the resulting margin expansion and debt-free balance sheet are likely to drive a sustained re-rating of the stock. TTL is no longer just a packaging company; but a Polymer giant in the high-stakes arena of the global energy transition.